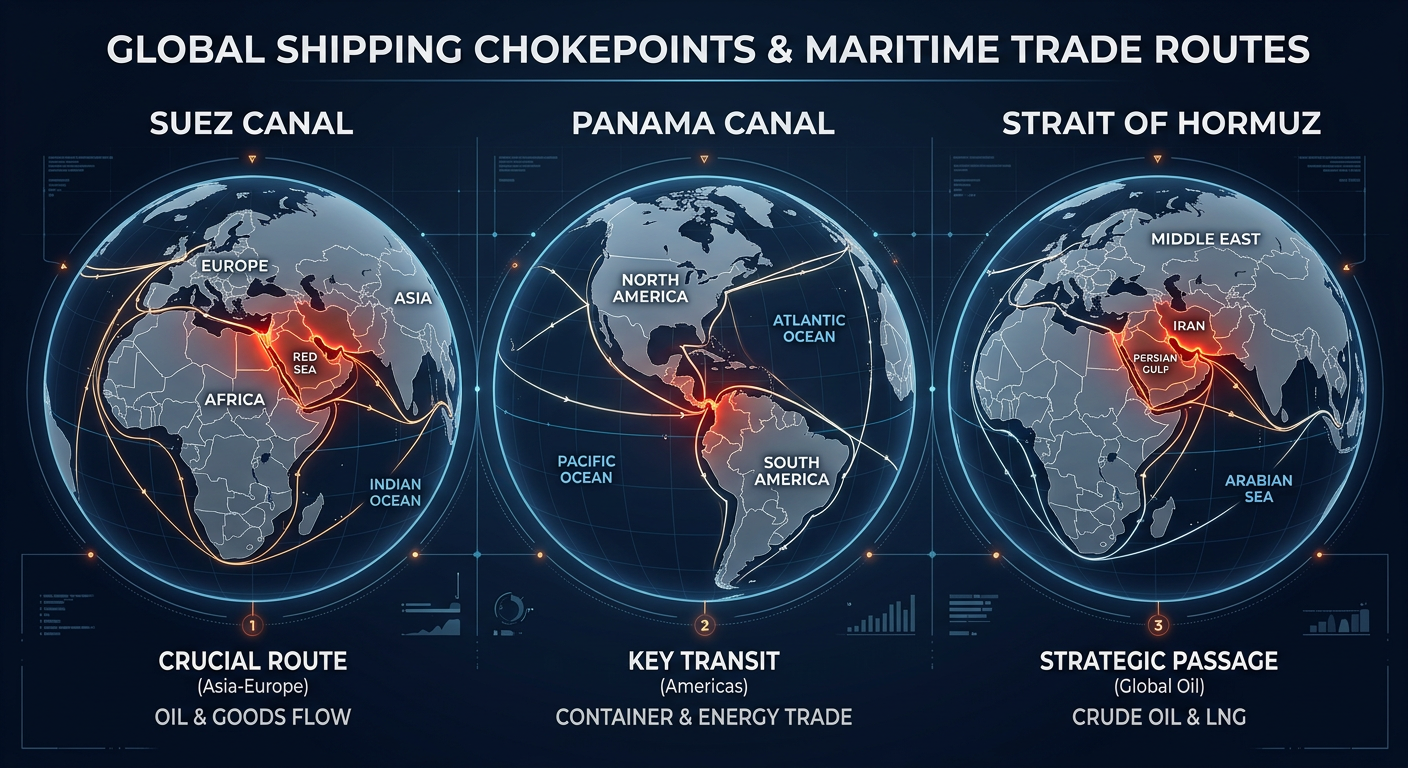

There are only a handful of places on Earth where geography forces the world's commerce through a bottleneck. The Strait of Hormuz, barely 21 miles across at its narrowest, handles a fifth of the planet's oil. The Suez Canal, a single artificial channel through Egyptian desert, carries 12-15% of international maritime trade. The Panama Canal, a system of locks cutting through 50 miles of Central American isthmus, connects the Atlantic and Pacific supply chains that keep the American economy functioning.

In a normal year, these three passages operate independently. A crisis at one can be partially absorbed by rerouting through the others, by drawing on strategic reserves, or by adjusting supply chains over weeks and months.

This is not a normal year. For the first time in the modern era of global trade, all three chokepoints are under significant stress simultaneously. The consequences for American consumers are compounding in ways that no single disruption has ever produced.

The State of Play: April 2026

Hormuz: Blocked. Following the launch of Operation Epic Fury on February 28, military operations in and around the Strait of Hormuz have reduced commercial oil transit through the strait by more than 90%. The U.S. Navy has imposed a blockade on Iranian ports. Iran's retaliatory posture, including mine-laying and the threat of anti-ship missile use, has made commercial insurers effectively unwilling to cover vessels transiting the strait without military escort. The result is a near-total shutdown of the world's most important energy corridor. Crude oil futures crossed $104 per barrel on April 12 when diplomatic talks in Doha collapsed.

Suez: Fragile Recovery. The Red Sea corridor, disrupted since late 2023 by Houthi attacks on commercial shipping, entered a tentative recovery phase in early 2026. Maersk resumed limited Suez transits in February after a partial ceasefire. But the recovery is patchy. CMA CGM, the world's third-largest container line, continues routing some services via the Cape of Good Hope. War-risk insurance premiums for Red Sea transit remain 5-10 times above pre-crisis levels. Any single Houthi attack could reverse the fragile progress overnight. The ceasefire holds, but it holds loosely.

Panama: Constrained. The drought that crippled Panama Canal operations in 2023-2024 has partially eased, but daily transit slots remain below the historical average of 36-38. The canal authority continues to impose draft restrictions that limit the maximum cargo weight per vessel, reducing effective capacity even for ships that secure transit slots. The canal is functional, but it is not operating at full capacity, and the backlog of demand from vessels rerouted from Hormuz and Suez is adding queue pressure.

Compound Effects: Why Three Is Much Worse Than One

When a single chokepoint is disrupted, the global shipping network adapts. Vessels reroute. Carriers adjust schedules. Costs rise, but the system absorbs the shock over 30-60 days.

When all three major chokepoints are stressed, the adaptive capacity of the network collapses. Every alternative route leads to another constrained passage or a dramatically longer journey. The arithmetic of compound disruption is brutal.

Consider a container of electronics components shipped from Shenzhen, China, to Newark, New Jersey. In normal conditions, this container might transit the Suez Canal and cross the Atlantic — a journey of approximately 30-35 days. If Suez is disrupted, the container reroutes around the Cape of Good Hope, adding 10-14 days and roughly $1 million in fuel costs per vessel. If Panama is also constrained, the alternative Pacific-to-Atlantic route via Panama faces queue delays. And the vessel's fuel costs are elevated because Hormuz disruptions have driven bunker fuel prices up 30-40%.

Each chokepoint disruption does not simply add to the others. They multiply. Longer routes mean more fuel consumed at higher prices. More vessels on longer routes mean fewer ships available for any given trade lane, tightening effective capacity. Tighter capacity means higher freight rates. Higher freight rates plus higher fuel costs plus longer transit times mean goods arrive later and more expensively — and the delay itself creates inventory shortages that give retailers pricing power.

The IMF published a working paper in February 2026 estimating that a 100-hour increase in average shipping time raises inflation by approximately 0.5 percentage points at its five-month peak, with the effect varying by product category and trade route exposure. We are currently experiencing average shipping time increases of 200-400 hours on the most affected routes.

Category-by-Category Impact Assessment

Fuel and Energy. The most immediate and severe impact. The Hormuz blockade alone removes approximately 17-20 million barrels per day of oil and petroleum product transit capacity (including products refined in Gulf states from Gulf crude). U.S. gasoline has already risen to $4.15 per gallon nationally, with the West Coast and Northeast above $4.50. If oil remains above $100 through Q2, expect gasoline to average $4.25-4.50 nationally through the summer — historically a period when prices rise due to seasonal demand. Heating oil and natural gas prices are also elevated due to LNG transit disruptions through Hormuz.

Groceries and Food. The transmission is slower but broad. Three channels are active. First, diesel-driven transportation costs are rising, adding 2-4% to the cost of moving food from farm to shelf. Second, fertilizer and agricultural input costs are rising with natural gas and petrochemical prices. Third, imported food — coffee, cocoa, seafood, olive oil, tropical fruits — faces higher shipping costs and longer transit times. The BLS Food-at-Home CPI index, which rose 1.8% year-over-year in February, is likely to accelerate to 3-4% by July as these cost pressures flow through.

Electronics and Consumer Goods. Container shipping from Asia to North America is doubly squeezed: by elevated fuel costs and by the effective loss of the Suez shortcut for Europe-Asia trade (which pushes vessels onto Pacific routes, competing for Panama Canal slots). Add the existing 30-55% U.S. tariffs on Chinese goods, and the landed cost of imported electronics, appliances, and household goods is at its highest point since the post-COVID supply chain crisis of 2021-2022. Expect selective price increases on consumer electronics, small appliances, and furniture through Q2-Q3 as retailers work through existing inventory and begin restocking at higher costs.

Apparel and Textiles. Heavily import-dependent (97% of clothing sold in the U.S. is imported) and sensitive to both shipping costs and cotton/synthetic fiber prices. Cotton futures have risen 15% since February on supply chain concerns and energy-cost-driven increases in synthetic fiber production costs.

The Tariff Multiplier

The compound shipping disruption arrives at a moment when U.S. trade policy is already adding friction to import costs. Chinese goods face cumulative tariffs of up to 55% (25% Section 301 + 20% fentanyl levy + 10% baseline). Every dollar of shipping cost increase is amplified by the tariff rate — a $100 increase in shipping costs on a Chinese product subject to 55% tariffs effectively becomes a $155 increase in landed cost before any retail markup.

This interaction between trade policy and supply chain disruption is rarely discussed in either trade policy analysis or shipping market commentary, but it is directly relevant to consumer prices. The tariff acts as a force multiplier on shipping cost inflation for Chinese imports, which represent the largest single source of U.S. consumer goods imports.

What the Indices Are Telling Us

Risk and Route's proprietary indices are designed to quantify exactly this kind of compound disruption.

The Route Disruption Index captures the aggregate stress across all three monitored chokepoints. In a normal period, the RDI hovers around 50. Preliminary readings suggest the current environment scores in the 75-85 range — the highest since the index's inception.

The Household Fuel Risk Index reflects the direct energy-cost exposure of American households. With crude above $100, Hormuz blocked, and no near-term resolution in sight, the HFRI is signaling elevated risk that gasoline prices will remain above $4 through the summer.

The Chokepoint Severity Scores for individual passages show Hormuz at critical levels, Suez at elevated but improving levels, and Panama at moderately stressed levels. The combination is what matters: when all three scores are elevated simultaneously, the compound effect on prices is 40-60% larger than any single score would suggest in isolation.

What to Watch

The next 30 days will be shaped by three variables.

Doha talks. Diplomatic negotiations between the United States, Iran, and intermediaries are scheduled to resume. Any progress toward a ceasefire or partial reopening of Hormuz would immediately relieve oil prices by $15-25 per barrel.

SPR decisions. The Biden administration has signaled willingness to release Strategic Petroleum Reserve barrels if prices remain elevated, but the current SPR level of approximately 370 million barrels limits the scale of any release. A 30-million-barrel release over 60 days would moderate gasoline prices by an estimated $0.10-0.15 per gallon — helpful but not transformative.

Red Sea stability. If the Houthi ceasefire holds through April and more carriers resume Suez transits, it would partially relieve the capacity pressure on Pacific routes and reduce the compound effect. A single high-profile attack on a vessel could reverse this progress entirely.

We will publish updated index readings and scenario analysis weekly through this crisis. The data will speak clearly even when the diplomatic situation does not.

The Evidence Box

Key Finding: Simultaneous disruption of Hormuz, Suez, and Panama is creating compound cost pressures 40-60% higher than any single disruption, with cascading effects across fuel, food, electronics, and apparel reaching American households over the next 60-120 days.

Supporting Data:

- Hormuz transit reduced 90%+, crude at $104.80/barrel — Bloomberg, CNBC

- Suez partially open but 5-10x insurance premiums persist — Container News

- Panama below historical transit capacity — Panama Canal Authority

- China-US container rates $3,400-$5,000/40ft + up to 55% tariffs — Gorto Freight

- IMF: 100-hour shipping delay = 0.5pp inflation at 5-month peak — IMF WP, Feb 2026

Confidence: High

What Would Invalidate: Rapid resolution of at least two chokepoint disruptions, or demand contraction offsetting supply-side pressure.